Automation of Tasks and Knowledge-Intensive Services: A Sectorial Approach to the Impact of Covid 19 in Argentina

; Julián Gabriel Leone***

; Juan Manuel Rodriguez Repeti****

; Julián Gabriel Leone***

; Juan Manuel Rodriguez Repeti****

Abstract

The covid 19 pandemic led to an economic collapse and multiple impacts upon Argentina's labour dynamics. As well as in other parts of the region, falls in employment rates (both due to an increase in unemployment and significant withdrawals from the labour force) were combined with wage reductions for those who were able to keep their jobs. Thus, two important processes for the labour market complimented each other: a structural shock associated with a tasks automation as a reorganisation and substitution of factors, with a cyclical recession caused by the pandemic. The international experience shows the amplifying impact the latter has on the former, generating long-term consequences mainly in routine-intensive jobs. However, the knowledge-intensive services sector appears to be the most capable of cushioning the recessionary shock (both in terms of wages and labour absorption), even with nuances within the sector depending on the extent of the shutdown measures and its capability to switch to remote work. Finally, the task approach is decisive in capturing the ability to adapt both the cyclical and structural processes, absorbing a large part of the explanatory potential that sectoral classifications tend to bring about.

La pandemia del COVID-19 supuso un colapso económico y múltiples impactos en la dinámica laboral argentina. Al igual que en el resto de la región, las caídas en las tasas de empleo (tanto por un aumento en la desocupación cómo por significativos egresos de la fuerza de trabajo) se sumaban a reducciones salariales para aquellos que pudieron conservarlo. Se complementaban así dos procesos de importante magnitud para el mercado de trabajo; un shock estructural asociado a la automatización de tareas y la reorganización y sustitución de factores, con una recesión coyuntural ocasionada por la pandemia. La experiencia internacional muestra el impacto amplificador que esta última tiene en la primera, generando consecuencias de largo plazo principalmente en aquellos empleos intensivos en tareas rutinarias. Sin embargo, el sector de servicios intensivos del conocimiento es el que mayores probabilidades presenta para amortiguar el shock recesivo(tanto a nivel remunerativo como en absorción laboral) aun con matices al interior de este de acuerdo con el grado de alcance de las medidas de cierre y la capacidad de migración al trabajo remoto. Por último, el enfoque de tareas resulta determinante para captar las capacidades de adaptación a ambos procesos, absorbiendo buena parte del potencial explicativo que suelen aglutinar las clasificaciones sectoriales.

Keywords:

Knowledge-Intensive Services, Automation of Tasks, Covid-19, Argentina, Market LabourServicios Intensivos del Conocimiento, Automatización de Tareas, COVID-19, Argentina, Mercado de Trabajo

Ⅰ. INTRODUCTION

The services sector has unique characteristics in terms of both job creation and productivity in the labour market, with results that do not always evolve in line with those of the economy as a whole. In particular, this paper is prepared in a context of macroeconomic adversity, after leaving behind the most complex consequences of the pandemic. However, its challenges are still far from being surmounted, and its culmination seems to extend in time, generating important and still uncertain effects on economies, both globally and locally. In this context, aspects related to the macroeconomic environment, sectoral development and its impact on the labour market are of particular standing. The challenges for societies and, above all, for governments due to the “day after” agenda of the pandemic are many, complex and even unknown. This is likely to be a transitional period in which the impact on labour dynamics caused by the restrictions imposed by each country through policies aimed at dealing with the health emergency will be gradually corrected.

This pape1r seeks to contribute to the post-pandemic crisis transition, with an emphasis on the recovery of societies' pre-pandemic living standards. This is done through a thorough analysis of the labour market dynamics produced by the crisis. Although a holistic view is proposed, the focus will be placed on a productive sector with features that do not always keep it in line with macroeconomic developments. Within the services sector, one section of industry stands out for becoming a user and producer of information and knowledge to provide services to its clients. These are the knowledge-intensive services1), which in recent decades have taken on a greater role in Argentina's productive structure and show a skilled labor demand, displaying, in some cases, a more agile ability for reconversion than other sectors in the face of the pandemic.

On the other hand, these services seem to combine a faster emergency readjustment to an unforeseen supply shock2), showing a better labour reconversion in response to structural technological shocks, mainly associated with the irruption of robotics and artificial intelligence. Thus, they seem to represent a virtuous impact in terms of factors substitution in the production function, in line with a pandemic crisis that modifies and increases labour transitions and trajectories.

Thus, an intersection analysis between types of industries and the labour market associates job characteristics with employment categories. However, within the same sector, the task that an individual actually performs may have considerable differences, thereby approximating a worker's skills and generating a precise correspondence among labour supply endowments and of labour demand requirements. As for the different effects of the pandemic on the labour market, some relevant trends could be listed: the destruction of jobs, the transformation of work tasks and the creation of occupations. This is no longer only the result of a technological revolution that makes it possible to replace work, but also of a crisis that differentiates essential occupations and forces a sudden migration to teleworking. For this reason, the aim is to investigate, within the knowledge sector, the tasks and individual characteristics that are most sensitive to these processes. At the same time, it seeks to understand the dynamics of labour paths associated with the combination of a structural and a circumstantial phenomenon that unleashes an unprecedented labour crisis.

Ⅱ. Framework

The knowledge-intensive services(KIS) sector stands out for overturning the characteristics generally assigned to the tertiary sector. While in general terms, its mention was a synonym for low productivity and scarce innovation, KIS industries are now recognised as bearers of productivity gains and knowledge spillovers both within the sector(Hipp & Grupp 2005; Miles et al. 1995; Schnabl & Zenker 2013) and for fostering it in various economic areas through the generation and diffusion of technological and non-technological innovations(Gotsch et al. 2011).

With significant qualities to become an engine of growth for the region, knowledge-intensive service industries are nowhere close to their potential yet(López & Ramos 2013). Their integration into the world's main value chains3) and global transnationalisation schemes makes the proliferation of the sector attractive for any economy, where, despite its uneven development4), its growth is not only limited to “rich” countries with high savings rates. In Latin America countries there is an increasing importance of KIS exports, in which for instance, Brazil is the largest exporter of market services, Argentina is the largest exporter of software services and Costa Rica is an important exporter of market and software services in the region(López & Ramos 2013; Méndez Maya et al. 2018). In particular, Argentina seems to present comparative advantages in the provision of these services(UNCTAD, 2018), even in spite of a decreasing performance in recent times.5) In terms of their morphology, Argentine CIS firms are larger than the national average (measured by number of employees) and tend to have higher wage expenditures than the overall mean(López & Niembro 2019). In addition, relative to other economic sectors, wages and social contributions represent a substantial part of the costs, reflecting the labour-intensive nature of these activities(López 2018). Nevertheless, a nodal feature for this paper is that aggregate labour characteristics may hide dissimilar sensitivities across CIS sub-sectors, and even heterogeneity within them(Amara et al. 2009; Consoli & Elche-Hortelano 2010; Corrocher et al. 2009).

In terms of labour dynamics, their development is strongly linked to the level of human capital of the country in which their services are offered(Chicha Mejía 2011)6), where different education indicators are one of the main determinants of their export ratios(Meyer 2007). Linked to high wages and value added, it is possible to account for the crucial role of(skilled) human resources in CIS and even the existence of certain conditions that allow in some sectors the emergence of extraordinary entrepreneurial income that can be partially absorbed by the respective labour force. Together with the business environment, this seems to be one of the main constraints for the region(López & Ramos 2018), and it should not be overlooked that the deficit of vocations in certain academic areas(such as engineering in general, or computing in particular), is becoming a widespread phenomenon in the West and is exacerbated in Latin America.

It is not only the human capital requirements a stylized fact that differentiate the sector. On the labour demand side, the tasks scheme that workers actually perform in their jobs also diverge from those performed in other segments, and within the sector the sensitivity to structural processes of technological change is uneven(Acemoglu & Autor 2011; Autor et al. 2003).7) Martinez et. al.(2020) shows the sector not only as a key part of the labour and productive scheme, but also as a driver of a complementary labour demand with new technologies whose productivity is accelerated by them.8) In contrast to traditional service sectors and goods industry, where the share of jobs intensive in routine and manual tasks(e.g. cleaning, hawking, etc.) was considerably higher, their risk of automation or of being included in the lower ranges of the income distribution became higher(Autor & Handel 2013).

In addition to the complex dynamics challenging the productive structures of the world's economies, an unprecedented labour crisis caused by Covid-19 is compounding trends that were already in progress prior to the arrival of the virus. The reduction in the level of economic activity in the region generates significant pressure on labour dynamics, which translates into a drastic employment, hours worked and labour income contraction. Both its impacts and the recovery path seems uneven according to sectoral adaptive capacities(Chernoff & Warman 2020)9), generating an amplification of labour and income gaps that may also disproportionately affect different population groups(Bartik et al. 2020)10) and exacerbate inequality levels existing before the outbreak of the pandemic(Beccaria et al. 2021). This is also driven by the rise of digital technologie(Czifra & Molnár 2020), which despite their ability to prevent collapse in the economy by ensuring a degree of connectivity, enact an excessive reconversion of tasks and production processes(Schilirò 2020).

Recent evidence from the US suggests that recessionary episodes promote both automation(expressed by robotics and artificial intelligence) and the relocation of productive resources as a way to increase efficiency and productivity in firms(Jaimovich & Siu 2020).11) Not only do routine jobs naturally suffer the greatest impact through job destruction, but also most of them are not generated again in recovery periods. The opposite is true for non-routinary occupations, which show much more subdued declines and quicker recoveries. In particular Kopytov et. al.(2018) point to the Great Recession as an enabler of this process, developing a model that explains the increase in the automation investment ratio for the period and the consequent labour polarisation. For the case of Canada, Blit(2020) reinforces this hypothesis by pointing out that the fall(and non-recovery) in the share of routine employment is discernible in the last three recessions, forecasting an even more pronounced impact in the covid crisis, and in industries that combine the greatest impact of shutdown measures and increased automation capacity.12) A stylised fact that is verified for both countries is that these dynamics coincide for the last recessions(since the mid-1980s after the start of the ICT revolution) as opposed to previous episodes.

At the same time, the features of this economic crisis make it dissimilar from previous downturns, being largely self-imposed through an unprecedented total economy shutdown economy as a way to mitigate the spread of the virus. Thus, both the trigger and the means of moderating its consequences make this crisis unique in its effects on the labour market. One of the main considerations is that unemployment rates cannot and fail to be a full measure of labour market difficulties. An aggregate measure requires the incorporation of reductions in activity rates, understood as a discouraging effect due to the impossibility to be hired. The latter has significant costs, given that transitions that migrate out of the labour force are those that make the process of returning to an occupation harder and longer(Kupets 2006).

Again, the addition of a focus on transitions between employment positions and wage dynamics points to the explanatory insufficiency of a single labour indicator(Cortes & Forsythe 2020). On the contrary, a first sectoral analysis should be nourished by a more specific framework such as a task approach that allows for an analysis of labour sustainability and reaction to structural changes(Acemoglu 2020). The inclusion of different individual characteristics must especially include an educational dimension, which is central to the knowledge sector(Schnabl & Zenker 2013). The need to understand and measure the specific impacts of the Covid-19 crisis on the labour market thus requires the inclusion of occupational and remunerative pathways for each of the sectors in relation to the particular characteristics of both labour supply and demand.13)

Ⅲ. Methodology

For this paper, data from the Permanent Household Survey(EPH) collected by the National Institute of Statistics and Censuses(INDEC) of Argentina is used, corresponding to the fourth quarter of 2019 and the fourth quarter of 2020, including those individuals which can be identified in both time periods. It should be noted that the EPH is carried out individually by surveying the person only once during a quarter, where in order to obtain the transition between tasks it is necessary to track them over time. For this, through a unique personal identification code, it is possible to do it for six quarters in a non-continuous way(a person is surveyed for two quarters) leaving a “resting” period. For this reason, a database is created from a balanced panel where the task is obtained in each of the individual's time observations.

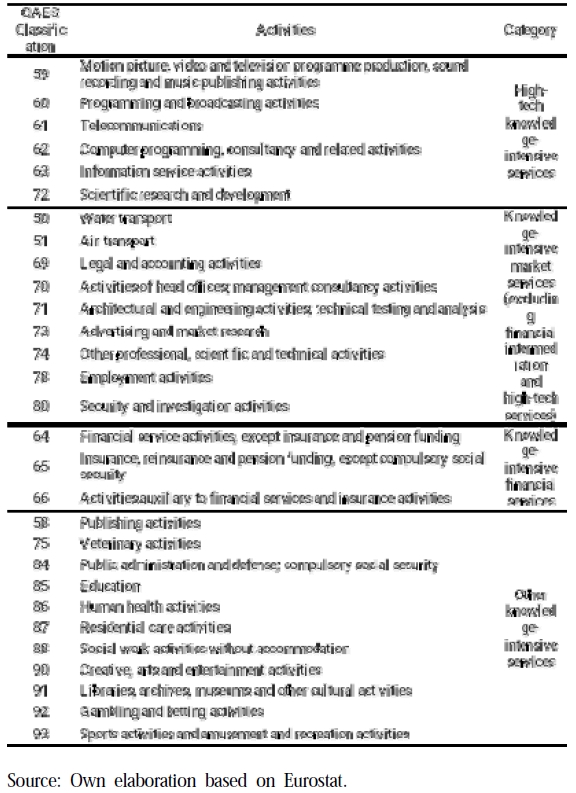

Subsequently, the different activities are grouped into goods- and services-producing sectors according to the Classification of Economic Activities for Socio-demographic Surveys(CAES). Within the latter, it is important to note that, in the literature on knowledge-intensive services, several definitions are proposed (García-Quevedo et al. 2013; Wood 2002), although empirically there is a consensus about the sectors that make up these types of services (Doloreux et al. 2008; Martínez et al. 2020; Schnabl & Zenker 2013; Torrecillas & Brandão Fischer 2011). With this in consideration, the activities corresponding to the different knowledge-intensive services are identified, and these activities were grouped by sub-sectors following the Eurostat classification14) (Table 1).15)

KIS classification (CAES)

Subsequently, using the typification of tasks for the different occupations set by the O*NET (Occupational Information Network), they are classified according to the task approach developed and used by Autor et al.(2003) and Acemoglu & Autor(2011). In this regard, four typical classifications of occupations consistent with the intensity of the tasks performed are determined by branch production branch: manual routinary (tasks associated with finger dexterity and the manipulation of small objects, performed by workers with medium qualifications but highly codifiable and replaceable by automation processes), manual non-routinary(involving low qualifications but not very codifiable, influenced by factors such as culture that make automation difficult), cognitive routinary(performed by workers with medium qualifications, which can be computerised due to their high repetition, such as tasks performed by administrative personnel, sales personnel, among others) and non-cognitive routinary(tasks performed by highly qualified staffs, which require abstract thinking, creativity, critical problem solving and communication skills, complemented by computing and technology).

In terms of statistical methods, firstly, a panel data was constructed to follow the same individuals over one year(IV2019-IV2020). A dummy variable takes value zero if the individual maintains his or her job and one if he or she lost it. Additionally, a dummy variable was constructed that takes the value zero if the individual's average wage remained above the average wage of the economy in real terms, and value one if it was below it.16) To explain the probability of these variables taking the value one, a Generalised Linear Model(GLM) is used for each case(Equation 1) using as controls geographical variables, age, gender, the branch of activity in which the individual is employed, the type of task performed, among others. The coefficients of the logistic regressions are estimated by maximum likelihood as a binary variable. Maximum likelihood estimators(MLE) are consistent, have minimal variance, and are normally distributed over large samples(Stock et al. 2012; Verbeek 2004). The estimated coefficients, once exponential, are interpreted as conditional odds ratios in a multiple regression. In addition, Pearson's chi2 test is performed for both models to test their goodness of fit. The predictive power of each model is also tested by means of the ROC(Receiver Operating Characteristic) curve and the area under it(AUC), reporting the same in the estimation of each model.

| (1) |

- • P(Y = 1|X)= Represents the probability that the dependent variable takes value one.

- •Xi= Represents the set of explanatory variables for both labour supply and labour demand.

- •βiβi= Represents the set of coefficients that accompany the explanatory variables.

- •β0= Is the estimation constant.

- •εi= Represents the estimation error.

Ⅳ. Descriptive Analysis

The magnitude of the pandemic's impact on the latin american labour market ranges from forced migration to telework, nominal wage reductions, and total inhibition of professions or services provision. A first inequality inequality was limited to dividing the population between those who maintain their income source and those who had already lost it, even worsening the high levels of inequality that existed before the outbreak of the pandemic.17) The latter were nurtured by different channels that differentiated the pandemic from other traditional crises. For Argentina, the unemployment rate returned to double digits (11%)18), a fact that was even cushioned by a massive outflow of the labour force19) (discouragement effect given the scarce job alternatives, a reduction in search incentives and the supply shock generated by the shutdown measures) having led to a higher level of unemployment.20) The employment loss reached almost 700 thousand workers21), of which more than 200 thousand were newly unemployed and almost 500 thousand had left the labour market, a fact that thwarts and lengthens the process of returning to a state of employment.22) At the same time, those who continued to earn an income did so in many cases on a partial basis. The remunerations present noticeable falls23), even if masked in general levels that did not show more pronounced declines, given that many of the jobs lost were located in the lower part of the income distribution.

However, the impact on employment and transitions within it match sectoral intensity. Undoubtedly, the knowledge-intensive services sector was the main mitigating factor in terms of employment retention, even with heterogeneities that cannot be captured by a standard statistical grouping. One of the main differences is observed in the market services sector, which includes activities that are more sensitive to the constraining process. Even within the classification, there is a notorious diversity with occupations whose effect on both the quantity and the wage impact 24) of the subgroup will be high. However, the knowledge sector differs from the goods industry and especially from the traditional services industry (with proximity personal services being the most affected). At the same time, the variation in hourly earnings shows a correlation with job dynamics. Even in a context of generalised loss of income, a fraction of CIS services(financial and high tech) show a wage evolution significantly above the evolution of prices. In contrast, the declines in the goods and services industries are in line with decreases in their labour absorption and are even tempered by the fact that most of the jobs lost were those with the worst hiring conditions.25) Again, the SIC sector does not behave uniformly, with certain professional services being prevented from migrating to telework, receiving a greater impact from the constraints of remoteness.26) (See Appendix I).

The unemployment rate only captures part of the magnitude of the difficulties faced by the labour market and therefore needs to be complemented by other labour indicators(Table A 1 and Table A 2). On the one hand, job losses are fuelled both by an increase in unemployment and a significant outflow from the labour force. On the other hand, the evolution of hours actually worked provides a more complete picture of labour market behaviour, reflecting not only job losses but also decreases associated with reductions in working hours or temporary suspensions. As can be seen in Graph 1, even among those who continue to maintain their employment, the reduction in hourly intensity is significant for almost all sectors.

Employment ratios variationSource: Own elaboration.

Regarding average income, it can be observed that the impact of the pandemic had negative consequences in most sectors, excluding services related to financial activities, which presented a real increase in average income and the category "Other SIC", where the average income managed to be situated just above the inflation line(Graph 2).

Real income variation by economic sectorSource: Own elaboration.

The exceptional situation of the pandemic multiplied the transitions witnessed in the labour market. The sharp fall in its volume implied transitions into unemployment and mostly pronounced exits from the labour force. At the same time, among those who remained in employment, high inter-sectoral movements were observed, with a significant outflow from the service industries(sectors mostly affected by the confinement and distancing measures, such as the leisure industry, commerce and non-professional personal services) to both knowledge sectors and the goods industry.

All this poses a complex challenge, where on the supply side, the activity level expresses a mild recovery that fails to reach pre-pandemic levels.27) Under this uncertainty, firms capability to rehire non-essential workers is low. Moreover, the literature presented here shows that for developed countries, a large part of these workforce is not reemployed, taking advantage of the opportunity to automate, reorganise operations and engender a factor reschedule. This process is not prompt, and the time it takes to readjust firms' production patterns can further exacerbate the recession. For example, factors such as labour and capital are relocated from proximity or materialisation tasks to online supplies and services(even within the same sector), a process that entails a delay in finding efficient levels of operations and scale. The Covid crisis differs from previous adversities in the degree of economic transformation induced. This translates into an unprecedented readjustment in firms' operations, with the drive to shift factors and task automation impacting disproportionately on both sectors and individual characteristics(Graph 3).

Tasks classification by economic sectorSource: Own elaboration.

Ⅴ. Results

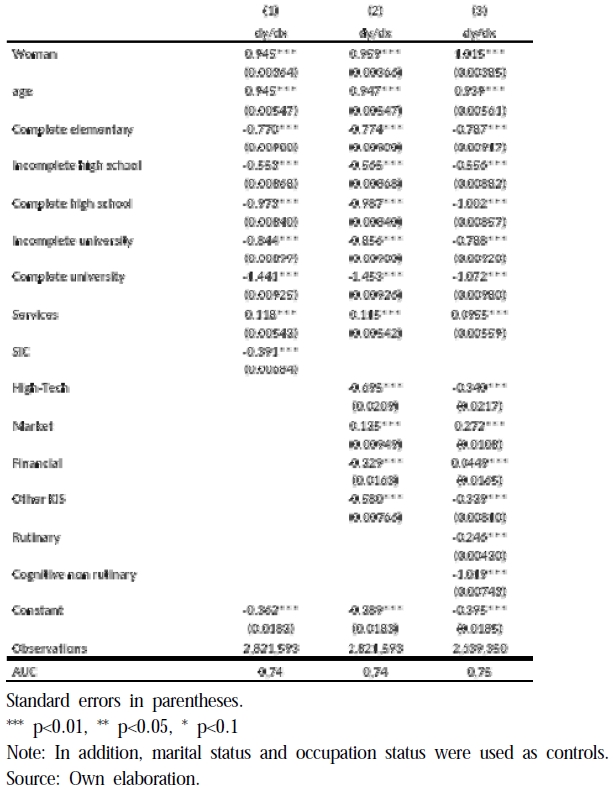

Regarding the employment loss for the period IV 2019 - IV 2020, it can be observed that women are more likely to be unemployed than men, thus widening the gender gaps in employment that existed prior to the pandemic. This is due to the fact that women tend to be employed in economic sectors that were strongly affected by the pandemic and by the lockdown measures. It is important to bear in mind that although the female labour force is overrepresented in education and health sectors(slightly affected by the crisis) this did not outweigh the loss of female employment in the remaining occupations. The same is true for young people compared to adults, with a higher participation in jobs linked to the hotel, leisure and construction sectors, among others, which were mostly affected by the closure measures. In addition, it can be seen that education is a determining factor for keeping the job, and that higher the education level in comparison with individuals who did not complete their primary school, lower the probability of job loss. These results are common to the three models, presenting different magnitudes in each of them, which are statistically significant at 1% (Table 2).28)

Job loss probability during pandemic

Breaking it down by sector, it can be concluded that individuals employed in the service sector have a 13% additional probability of becoming unemployed according to the first two models(Table 2, columns (1) and (2)), and 10% under model three(Table 2, column (3)), compared to an individual employed in the goods-producing sector. In contrast, individuals employed in the SIC sector have a 37% higher likelihood of remaining employed than those employed in the goods-producing sector.29)

Within the KBIS, the only subgroup with a higher probability of job losses(between 14% and 26%) compared to the production of goods, is the Knowledge - intensive market services subgroup, which is an interesting but predictable result. This subgroup includes tasks such as Water and Air transport, Architectural and engineering activities, among others, activities that have been affected negatively by the pandemic(Table 2, columns (1) and (3)).30)

The addition of task controls groups together much of the explanatory potential previously attributed to sectoral disaggregation. In line with previous studies(Martinez et. al. 2020), while sectoral differentiation is useful for a projection analysis, a further in-depth analysis at the individual task level has an even higher explanatory power, even after controlling for educational levels. In short, a purely sectoral analysis seems to be an incomplete solution when it comes to a thorough diagnosis of the labour map and its sensitivity to recessionary episodes. In line with this, it is noted that routine manual and non-routine cognitive tasks present lower probabilities of job loss, 24% and 100% respectively, these results being statistically significant at 1%(Table 2, Column (3)).

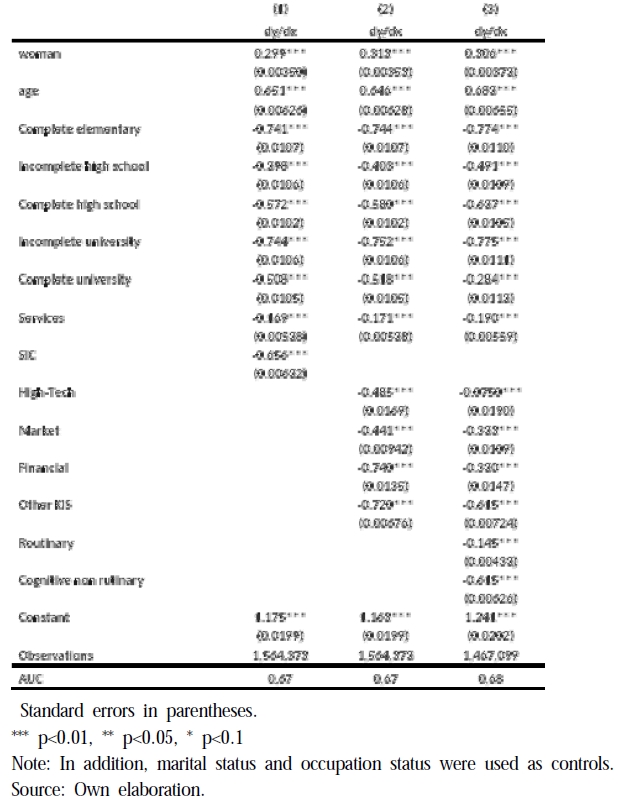

In terms of individuals' wages, the real variation of hourly income shows a reduction31) for women compared to men in all three estimated models. In addition, the real hourly income of adults is less likely to decrease compared to that of young people. Additionally, it is observed that the higher the educational level, the lower the probability for real hourly income to decrease. These results are common to all three models and are statistically significant at 1%.

As for services, in the three estimated models it can be observed that there is a lower probability that the real hourly wage will be reduced in relation to that of goods(around 17%), depending on the model. In addition, the hourly wages of KIBS have a nonreduction probability of 66% compared to those of goods. Within the CIS, all the subgroups present negative probabilities of real hourly income reduction compared to individuals employed in the goods sector, these results being statistically significant at 1%. Finally, if we look at the tasks performed in the different productive activities, routinary manual tasks have a probability close to 15% of having a decrease in their hourly wage in real terms with respect to non-routinary manual tasks, and in non-routinary cognitive tasks this probability is around 61%(Table 3).

Real Income decrease probability during pandemic

Ⅵ. Conclusion

The Covid 19 pandemic persists in breeding health difficulties at the same time this research is being written. However, its deeper economic impact appears to have been surmounted, leaving several conclusions and lessons for future research questions and policy directions. The collapse in the labour market was unprecedented in its speed of decline, while its recovery was partial, discontinuous and subject to characteristics and conditions of both labour supply and demand. Many firms had to cease operations and did not resume them, while many workers could not be rehired and, in several cases, even dropped out of the labour force.

The extent of the recession, however, was not homogeneous, deepening a clear sectoral cleavage, and specifically, according to the tasks performed. Undoubtedly, the traditional service sectors were the hardest hit, being the first to receive the shock of sanitary restrictions and the impossibility of contact. This phenomenon was credited to a higher extent than in goods and manufacturing sectors associated with higher specific human capital linked to experience in the firm. Workers in these industries were significantly more likely to lose their jobs, and among those who kept it, their chances of listing a wage reduction above the economy average were even higher. In this way, the knowledge sector was the most adaptable to a process of forced migration to telework, including many activities not exempted from the isolation restrictions, declared as essential. However, even within the knowledge sector, its performance could not be standardized. Serious effects are observed in sectors with total business interruption and no capacity for remote service provision.

Following the literature, recessionary shocks generate disproportionate impacts depending on the type of tasks performed, accelerating structural processes linked to the reconversion and substitution of work. There were tasks priorly threated and sectors with serious challenges before the pandemic, and which to a greater extent bore the burden of previous recessions. These same jobs, principally located in the lower tail of the income distribution (non-routine manual) and those with the highest risk of automation (routine), are the ones that are significantly more likely to exit employment rates and reduce their real income. Although these effects are mainly observed for the former (many of them associated with informal employment and low educational achievements), for the latter the risk of job extinction is higher, even if pre-crisis levels are recovered. Thus, the growth in automation and demand for skilled labour is accelerated by the depth of recessions, a trend that translates almost entirely into permanent losses in routine employment. These periods of urgent reorganisation for companies production function can generate long-term impacts on both firm productivity and the associated labour markets. Within this framework, any public initiative should be considered, assessing its capacity to promote collective welfare by mitigating the multiple adverse effects on the labour market.

Acknowledgments

Paula Maliniauskas & Bautista Bassi (fellow research assistants).

Notes

References

- Acemoglu, D.(2020), Remaking the Post-COVID World. Sixth Richard Goode Lecture.

-

Acemoglu, D., & Autor, D.(2011), “Skills, Tasks and Technologies: Implications for Employment and Earnings”, In Handbook of Labor Economics, Vol.4, pp.1043-1171.

[https://doi.org/10.1016/S0169-7218(11)02410-5]

- Elsevier. https://doi.org/10.1016/S0169-7218(11)02410-5

-

Amara, N., Landry, R., & Doloreux, D.(2009), “Patterns of innovation in knowledge-intensive business services”, The Service Industries Journal, Vol.29, No.4, pp.407–430.

[https://doi.org/10.1080/02642060802307847]

-

Autor, D. H., & Handel, M. J.(2013), “Putting Tasks to the Test: Human Capital”, Job Tasks, and Wages, Journal of Labor Economics, 31(S1), S59-S96.

[https://doi.org/10.1086/669332]

-

Autor, D. H., Levy, F., & Murnane, R. J.(2003), “The Skill Content of Recent Technological Change: An Empirical Exploration”, The Quarterly Journal of Economics, Vol.118, No.4, pp.1279-1333.

[https://doi.org/10.1162/003355303322552801]

-

Bartik, A. W., Bertrand, M., Lin, F., Rothstein, J., & Unrath, M.(2020), Measuring the labor market at the onset of the COVID-19 crisis. National Bureau of Economic Research.

[https://doi.org/10.3386/w27613]

-

Beccaria, L., Maurizio, R., Trombetta, M., & Vázquez, G.(2021), “Short-term income mobility in Latin America in the 2000s: Intensity and characteristics”, Socio-Economic Review.

[https://doi.org/10.1093/ser/mwaa043]

-

Blit, J. (2020). “Automation and Reallocation: Will COVID-19 Usher in the Future of Work?”, Canadian Public Policy, 46(S2), S192–S202,

[https://doi.org/10.3138/cpp.2020-065]

-

Chernoff, A. W., & Warman, C.(2020), COVID-19 and Implications for Automation’, No. W27249. National Bureau of Economic Research [Online].

[https://doi.org/10.3386/w27249]

- Chicha Mejía, J. E. (2011), Definición de los sectores económicos intensivos en conocimiento a partir de la clasificación que hace la OCDE y el análisis del nivel de cualificación de los trabajadores: Análisis para Catalunya.

-

Consoli, D., & Elche-Hortelano, D.(2010), “Variety in the knowledge base of Knowledge Intensive Business Services”, Research Policy, Vol.39, No.10, pp.1303-1310.

[https://doi.org/10.1016/j.respol.2010.08.005]

-

Corrocher, N., Cusmano, L., & Morrison, A.(2009), “Modes of innovation in knowledge-intensive business services evidence from Lombardy”, Journal of Evolutionary Economics, Vol.19, No.2, pp.173-196,

[https://doi.org/10.1007/s00191-008-0128-2]

-

Cortes, G. M., & Forsythe, E.(2020), Impacts of the COVID-19 Pandemic and the CARES Act on Earnings and Inequality.

[https://doi.org/10.17848/wp20-332]

-

Czifra, G., & Molnár, Z.(2020), Covid-19 and industry 4.0. Res. Pap. Fac. Mater. Sci. Technol. Slovak Univ. Technol, 28(46), pp.36–45.

[https://doi.org/10.2478/rput-2020-0005]

-

Doloreux, D., Amara, N., & Landry, R.(2008). “Mapping Regional and Sectoral Characteristics of Knowledge-Intensive Business Services: Evidence from the Province of Quebec (Canada)”, Growth and Change, Vol.39, No.3, pp.464-496.

[https://doi.org/10.1111/j.1468-2257.2008.00434.x]

-

García-Quevedo, J., Mas-Verdú, F., & Montolio, D.(2013), “What types of firms acquire knowledge intensive services and from which suppliers?”, Technology Analysis & Strategic Management, Vol.25, No.4, pp.473-486.

[https://doi.org/10.1080/09537325.2013.774348]

- Gotsch, M., Hipp, C., Gallego, J., & Rubalcaba, L.(2011), “Sectoral innovation watch: Knowledge intensive services sector”, Europe INNOVA Sectoral Innovation Watch, for DG Enterprise and Industry, European Commission.

-

Hershbein, B., & Kahn, L. B.(2018), “Do recessions accelerate routine-biased technological change? Evidence from vacancy postings”, American Economic Review, Vol.108, No.7, pp.1737-1772.

[https://doi.org/10.1257/aer.20161570]

-

Hipp, C., & Grupp, H.(2005), “Innovation in the service sector: The demand for service-specific innovation measurement concepts and typologies”, Research Policy, Vol.34, No.4, pp.517–535.

[https://doi.org/10.1016/j.respol.2005.03.002]

-

Jaimovich, N., & Siu, H. E.(2020), “Job polarization and jobless recoveries”, Review of Economics and Statistics, Vol.102, No.1, pp.129-147.

[https://doi.org/10.1162/rest_a_00875]

-

Kopytov, A., Roussanov, N., & Taschereau-Dumouchel, M.(2018), “Short-run pain, long-run gain? Recessions and technological transformation”, Journal of Monetary Economics, 97, pp.29-44.

[https://doi.org/10.1016/j.jmoneco.2018.05.011]

-

Kupets, O. (2006), Determinants of unemployment duration in Ukraine. Journal of Comparative Economics, Vol.34, No.2, pp.228-247.

[https://doi.org/10.1016/j.jce.2006.02.006]

- López, A. (2018). Los servicios basados en conocimiento:¿ Una oportunidad para la transformación productiva en Argentina. Documento de Trabajo Del IIEP, 31.

-

López, A., & Niembro, A.(2019), La Heterogeneidad de los Servicios Intensivos en Conocimiento: El Caso de Argentina. Journal of Technology Management & Innovation, Vol.14, No.4, pp.85–99.

[https://doi.org/10.4067/S0718-27242019000400085]

- López, A., & Ramos, A.(2018), El sector de software y servicios informáticos en la Argentina. Evolución, Competitividad y Políticas Públicas. Argentina: Fundación CECE. Recuperado De.

- López, A., & Ramos, D.(2013), ¿ Pueden los servicios intensivos en conocimiento ser un nuevo motor de crecimiento en América Latina? Revista Iberoamericana de Ciencia, Tecnología y Sociedad-CTS, Vol.8, No.24, pp.81–113.

-

Martínez, R. G., Leone, J. G., & Rodriguez-Repeti, J. M.(2020), “Morfología del empleo en las industrias de servicios intensivos en conocimiento. El caso de la Ciudad Autónoma de Buenos Aires”, Revista Escuela de Administración de Negocios.

[https://doi.org/10.21158/01208160.n0.2020.2740]

-

Méndez Maya, A. S., de Hidalgo, N., & Figueroa, E. G.(2018), “Competitividad del comercio internacional de servicios intensivos en conocimiento de México, Chile, Colombia, Costa Rica y Brasil”, Mercados y Negocios, 1(37).

[https://doi.org/10.32870/myn.v0i37.7088]

- Meyer, T.(2007), India’s specialisation in IT exports: Offshoring can’t defy gravity. Research Notes.

- Miles, I., Kastrinos, N., Flanagan, K., Bilderbeek, R., Den Hertog, P., Huntink, W., & Bouman, M.(1995), Knowledge-Intensive Business Services: Users. Carriers and Sources of Innovation, EIMS Publication, 15.

-

Rodriguez Repeti, J. M., & Marcel, L.(2021), “Mercado Laboral, Servicios Intensivos en Conocimiento y Género: Análisis para el Caso Argentino”. Journal of Technology Management &Amp; Innovation, Vol.16, No.3, pp.57–65.

[https://doi.org/10.4067/S0718-27242021000300057]

- Schilirò, D. (2020), Towards digital globalization and the covid-19 challenge.

- Schnabl, E., & Zenker, A.(2013), Statistical classification of knowledge- intensive business services (KIBS) with NACE Rev. 2. Fraunhofer ISI Karlsruhe.

-

Torrecillas, C., & Brandão Fischer, B.(2011), “How Attractive are Innovation Systems for Knowledge Intensive Services’ FDI?: A Regional Perspective for Spain”, Journal of Technology Management & Innovation, Vol.6, No.4, pp.45-59.

[https://doi.org/10.4067/S0718-27242011000400004]

- UNCTAD (Ed.)(2018), Investment and new industrial policies. United Nations.

-

Wood, P. 2002), Knowledge-intensive Services and Urban Innovativeness. Urban Studies, 39(5–6), pp.993-1002.

[https://doi.org/10.1080/00420980220128417]

Appendix

Appendix I.

Labor Transitions (from file to column)

Labor Transitions (from file to column)